Many people are not ready to be business owners. They don’t have the financial literacy to balance a checkbook let alone read their balance sheet. Or they are in debt from the day they graduate high school until the day they die–forever paying interest that would be better used to generate income. If you hope to have a sustainable business then it starts with being in command of your personal finances.

As an aspiring entrepreneur, you are jumping into a world of uncertain income. That is a scary proposition and not a decision to take lightly. The money you save before taking the plunge will be what keeps a roof over your head and ramen in your bowl. The financial habits you build now will help determine whether you succeed or fail as an entrepreneur.

Startup runway

Entrepreneurs are optimists by nature–if we were not we would not be making the leap–but the fact is that most of our early revenue projections are going to be wrong. It will likely take you many more months, if not years, than you expect to get to a point where your business is able to provide the income that you and your family require.

The reasons that people become entrepreneurs differ. Some of us start our businesses out of a desire to control our own destiny or as a way to build wealth. Others do it out of necessity when the income from their job is not enough to cover their expenses. Regardless of the reason that you take the journey down the entrepreneurial path, the road is going to be difficult and filled with obstacles.

Building up savings is one of the best ways to give yourself the freedom to focus on overcoming those obstacles. The more savings you have the longer your runway and the more time you have to talk to customers, iterate on your product, test marketing strategies, and ultimately find a repeatable way to generate income.

Budgeting is the basis of a financial plan and a key to achieving financial wellness. It will help you build you runway and ultimately find success. When you budget you take the planning that you are doing for your business and apply it to your personal finances. Until your business is self-sustaining your business finances and personal finances are linked and you need to do your personal and business bookkeeping regularly and meticulously.

Creating a budget

As an entrepreneur, you are well-versed with spreadsheets (if not then drop everything and learn Excel) so I suggest starting there with your budgeting.

In the first column list all of your spending categories. Start with the following:

- Housing

- Rent/Mortgage

- Electricity

- Gas

- Water

- Trash

- Sewer

- TV/Internet

- Home maintenance

- Living

- Groceries

- Dining

- Clothing

- Hair/nails

- Household Goods

- Entertainment

- Medical

- Telephone

- Vehicles

- Fuel

- Vehicle Maintenance

- Auto Insurance

- Giving

- Charity

- Gifts

- Miscellaneous

- Bank Fees

- Miscellaneous

- Business

- Debt

- Credit Cards

- Student Loans

- Auto Loans

- Other Debt

- Savings

- Emergency Fund

- Retirement

- Runway

- Other Goals

In creating categories you can either error on the side of fewer categories (spend less time categorizing expenses as you enter them) or more categories (drill down to where you are overspending and have opportunities to save).

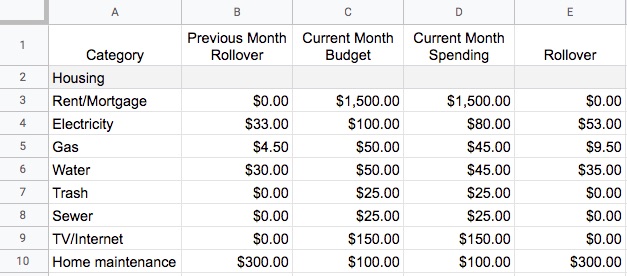

Create four columns next to the categories. The first column will be the previous month rollover which in this case will be $0. The second column is this month’s budget amount. The third column tracks your actual spending. The fourth column is the difference (Previous Month Rollover + Current Month Budget – Current Month Spending).

When entering your budget you must abide by a few rules:

- You cannot budget more spending than you have income.

- Every dollar of income must be budgeted.

- Use a “rollover” category to allocate any money you don’t budget this month for next month.

- You want to get to the point where you are using the income from previous months to pay this month’s expenses.

The runway category is where you should concentrate your savings once you have funded your emergency fund. It is also critical to pay off any credit card debt you have prior to making the leap to full-time entrepreneurship. That is an anchor that will drown your business before it can float.

Tracking Spending

Building the budget is the first, and easier, part of the budgeting process. The second step is to track your spending throughout the month. By doing this you will be aware of how much you have spent, and how much you have remaining, in each budget category. The effect is that you will start questioning yourself each time you spend money and ultimately make fewer impulse purchases. You will be less likely to sign up for the latest SaaS product that you think you need (but probably don’t) or you might look longingly at a new phone while thinking about how many Google ads you can buy for that money.

Proactively track your spending using another tab in your spreadsheet. Enter each receipt and use a formula so that the spending column on the budget tab is automatically updated. For your transactions tab I recommend the following columns:

- Account Name

- Payee

- Category (matching up to the category name in your budget)

- Transaction Date

- Amount

- Note

Remember to track all spending which is the money that goes out the door from your checking account, savings account, and any credit cards you have.

You can also use one of the many budgeting sites or apps for this. Those apps connect to your bank and credit card accounts and pull the transaction data so that you are not manually entering the transactions. This is a reactive approach to budgeting as you need to remember to check the app on a regular basis. I recommend doing so at least twice a week so you are always aware of how much money you have left in each budget category. Friday, before you go out with friends and do your weekend shopping, and Monday, so you can plan your spending for the week.

Monthly review

On the last day of every month, do a monthly review of your budget where you take stock of what categories you spent less than you budgeted and where you went over (hopefully nowhere!). This process will only take ten minutes if you have been good about tracking your spending throughout the month.

Combine your budgeting review with a monthly review of your business where you set definitive business goals for the next month and review what you have accomplished in the past month.

These reviews are essential for maintaining a view of the big picture when you are head down in the weeds most days. They ensure that you are pointed in the right direction and making progress. As you build good budgeting and business habits you will see your trajectory increase and your business take off–leaving the runway worries behind.